There were 348 SPACs scheduled to expire in 2023 as of February 7, 2023. 92 SPACs holding trust accounts worth over $26 billion (bn) are required to finalise mergers alone in the month of March. Blank check corporations are under a lot of pressure to finish business combinations because of impending expiration deadlines. 19 SPACs with more than $5 billion in trust have already liquidated as of February 7, 2023, as opposed to 0 liquidations during the same period in the previous year. SPACs looking for targets in the technology, media, and telecoms (TMT) sector have accounted for the majority of 2023 liquidations thus far.

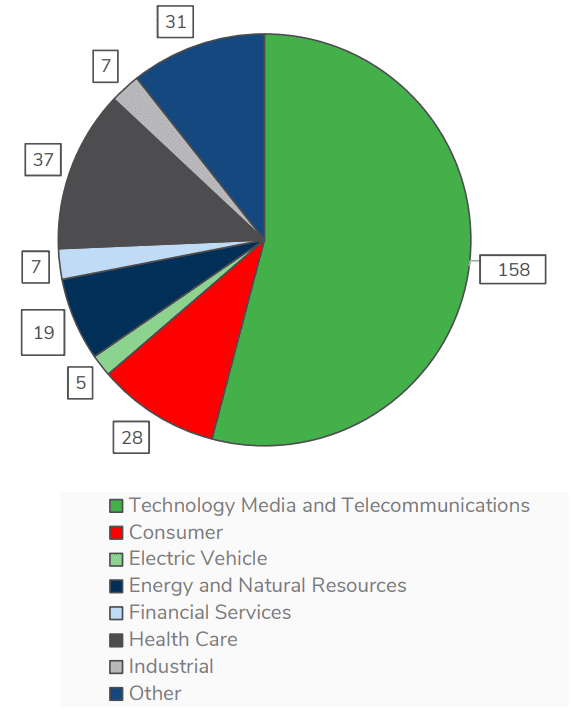

Number of SPACs Looking for Targets by Sector

In 2023, there will still be 158 TMT-focused SPACs with trust values over $40 billion that aim to combine. SPACs will probably have more liquidations in 2023 than in 2021 and 2022 combined, given the existing status of the industry.

With a record number of liquidations in 2022 and an 85% decrease in IPOs from 2021, the SPAC market saw a dramatic downturn in 2022. From $265 million (mn) in 2021 to $156 million (mn) in 2022, the average size of an IPO decreased. In addition, there were 142 liquidations in 2022 as opposed to only one in 2021, and the average redemption rate increased by over 100%. SPACs have several obstacles to overcome, such as tighter regulations, a deteriorating stock market, and rising interest rates. These challenges make the market even more competitive, with over 380 SPACs looking for targets.

SPACs Looking to Achieve a Target Trust Amount by 2023 Expiration (mm)

2022 SPAC Market Transaction Activity

![]()

2022 Executive Summary: Industry-specific Median De-SPAC Share Percent Return (2009-2022)

Important note:

SPAC Consultants is not offering and/or providing investment advisory services in the sense of regulated investment advisory services as per respective EU Directives and their implementation into national law of EU Member States. Instead, SPAC Consultants offers SPAC Project Management services and consults regarding the general principles of US SPACs and their business structuring. Any investment, legal and financial advice that may become necessary for possible sponsors and investors at advanced stages will be provided by the network partners of SPAC Consultants.

The FSAC SPAC will be focusing on established companies in North America that are growing significantly and have positive cash flow plus strong margins; FSAC’s target valuation is $500m to $2b.

FinTech is in the beginning stages of transforming the global financial and investment business. There has been a rise in the level of sophistication and interconnectivity between innovative technology and financial services providers and we expect this trend to continue and accelerate.

North America was the leading revenue contributor to the global business in 2019 and is presumed to continue its dominion in the coming years as well which can be attributed to increased adoption and development of prominent technologies in the fintech sector in the region.

The global financial technology market is expected to grow gradually and reach a market value of approximately $ 305 billion by 2025, growing at a compound annual rate of about 22.17% in the same period.

The global Foreign Exchange market is currently experiencing a healthy growth. Looking forward, the market is expected to register a CAGR of around 6% during 2020-2025.

The outstanding CEO and entire Management Team of FSAC has successfully built multi-billion dollar publicly-held financial technology companies, designed and developed cutting-edge technology platforms in the financial services sector on Wall Street.

The FSAC SPAC presentation:

SPAC Consultants: Our holistic approach to SPACs

As experienced SPAC consultants or SPAC advisors, we provide our SPAC advisory and project management services to different group of clients related to SPACs.

Our SPAC consulting and project management services are tailor-made for private equity investors who wish to invest in their own SPAC on the pre-IPO stage as so-called SPAC Sponsors, or who prefer to sponsor an existing SPAC project at its pre-IPO stage.

As SPAC consultants, we are designing and structuring SPACs, arranging for S.E.C. approval and listing at Nasdaq or NYSE, organising pre-IPO roadshows, arrange for IPOs and assist in finding acquisition targets as per a SPAC’s acquisition strategy. Our SPAC consultants and advisers are well experienced on all stages and aspects of SPACs.

If you are interested in setting up a SPAC or in participating in an existing SPAC on its pre-IPO stage, we will be happy to arrange an initial Zoom conference to get acquainted, to further elaborate on SPACs and their manifold opportunities, and to discuss with you your SPAC investment and business ideas.

Important note:

SPAC Consultants is not offering and/or providing investment advisory services in the sense of regulated investment advisory services as per respective EU Directives and their implementation into national law of EU Member States. Instead, SPAC Consultants offers SPAC Project Management services and consults regarding the general principles of US SPACs and their business structuring. Any investment, legal and financial advice that may become necessary for possible sponsors and investors at advanced stages will be provided by the network partners of SPAC Consultants.

In this article, we will briefly analyse the financial mechanics of the proposed deal, which still needs to be approved by the IPO shareholders of Queen’s Gambit.

Queen’s Gambit’s IPO and Acquisition Strategy

Special Purpose Acquisition Company Queen’s Gambit Growth Capital’s planned to raise $300 million during its IPO. Its Book Running Manager Barclays used its option for over-allotment and upsized the IPO to $345 million. The SPAC floated its IPO on 20th of January 2021.

With $345 million in trust, a SPAC typically looks for acquisition target companies with a valuation of $1.035 to $1.725 billion.

In its S-1 filed with the SEC, Queen’s Gambit Growth Capital did not provide a concrete direction of its acquisition strategy, saying “We intend to focus our search on a target business that provides solutions promoting sustainable development, economic growth and prosperity.”

The SPAC’s sponsor is Queen’s Gambit Holdings LLC, which is controlled by Ms. Grace and owned by members of its management team and board, its Advisory Board, an affiliate of Agility and certain other individuals.

Queen’s Gambit’s Proposed Business Combination and Transaction

Queen’s Gambit valuated Swvl at $1.133 billion, which is 2.8x its 2023E gross revenue.

Queen’s Gambit is holding in its trust account $345 million cash (proceeds from IPO with over-allotment).

PIPE investors will provide additional $100 million, bringing the total cash available to $445 million.

After Swvl has been merged into Queens’s Gambit SPAC, it will receive the total of available cash, being $ 445 million.

Of this amount, $40 million will be used to cover the expenses and fee to close the transaction and list on NASDAQ, remaining operation capital for Swvl will be $405 million.

The above figures show that the shareholders of Swvl will be 100% compensated with a share swap, no cash pay-outs to the shareholders from IPO proceeds). Abstaining from any cash-outs for themselves from the available cash, Swvl’s shareholders fully support maximum operation capital for to company, thus showing their commitment to stay and to further develop the company’s business as soon as possible.

Queen’s Gambit Growth Capital will hold 6% of the shares of the post-merger company.

Who Are the Shareholders of Swvl and How Will They Benefit?

The founders of Swvl are well-known meanwhile, as they appeared on public media everywhere. But who are the other shareholders of the company?

The shareholders of Swvl comprise the following group:

- Founders

- Employees

- Investors

Swvl’s Founders

Swvl was co-founded by Mostafa Kandil in early 2017 when he was just 24 years old, together with Mahmoud Nouh and Ahmed Sabbah, who were even younger. They set up their company putting together their personal savings, $30,000. Mostafa is the CEO of the company. As Mostafa is the biggest individual shareholder in the company, assumingly – details are not known yet – he will hold at least several 10 million dollars in form of equity, if the proposed deal gets approved by the IPO investors.

Mahmoud left the company in October 2019 but kept his shares. It is not known yet whether his shares will be acquired during the acquisition or if he remains as a shareholder.

Ahmed left the company in 2021, after more than 4 years. He is expected to have his fair share.

Swvl’s Employees

Swvl knows how to motivate its employees. Many of them, together with executives, have been given stock options. Provided that they execute their stock options when the company goes public, they will earn millions.

Founder and CEO Mostafa Kandil wrote in a public post announcing the planned SPAC merger: “Today, Swvl hasn’t only created a monumental everlasting impact on the region, but also a life-changing impact for everyone within. We will soon have USD 18 millionaires, AED 95 millionaires, and EGP 203 millionaires of our colleagues, which I am sure will soon start the world’s Swvl Alumni Mafia.”

Swvl’s Investors

Back in Spring 2017, Swvl had a difficult start; nobody believed in their project and mission, possible investors approached by the founders did not show interest. But in July 2017 Swvl received a cheque of $500,000 from Careem, a Dubai-based subsidiary of the American company Uber. This was the kickstart for Swvl, and nobody could hold them back.

In return, Careem received 20-25% of Swvl’s shares, the exact figure is not known. Less than a year later, Careem was bought out by Series A investors. Had Careem held its shares, it could have generated a return on investment of over 700 times, post SPAC merger.

Series A investors were mainly funds from the region. During the next four years, Swvl raised more that $100 million from funds, VCs and other investors, who are now all shareholders and will benefit from the upcoming merger; namely:

- Beco Capital

- Vostok New Ventures

- Silicon Badia & Digame

- Arzan VC, Raed Ventures, Oman Technology Fund, and Sawari Ventures

- Other institutional investors

- Individual investors

Beco Capital

Beco Capital, co-founded by Dany Farha and based in Dubai, provides growth capital and hands-on operational support for early-stage technology companies, with the vision is to reinvent the Middle East through innovation and tech. Beco Capital has invested in more than 23 companies in the MENA region.

Beco Capital did co-lead the Series A funding round in February 2018 and invested itself. The Series A round provided Swvl with $8 million fresh funds. Beco Capital did also co-lead Swvl’s later funding rounds. It was mainly thanks to Dany Farha’s efforts that Swvl was able to raise $100 million, through several funding rounds. Dany is a board member of Swvl. Other than the unicorn Swvl, Beco Capital backed two other unicorns in the region at its early stages: Careem and Kitopi.

Considering it pivotal role, Beco Capital is expected to own a significant stake in the company and thus will provide its limited partners with a very heathy return on investment.

Vostok New Ventures

Vostok New Ventures, a Swedish Venture Capital firm, did co-lead the Series B-2 round in June 2019 which raised $42 million, and also invested itself. Vostok New Ventures continued investing during later funding rounds an now owns 12.5% of Swvl’s shares. Their shares will probably have a value of over $110 million after the merger. However, their ROI will be lower than Beco’s return, as they entered the company at a higher valuation that Beco.

Silicon Badia & Digame

Silicon Badia and Digame Investment did co-lead the Series A and B-1 funding rounds, together with Beco Capital. Silicon Badia is based in New York and Amman, while Digame is based in London, with its investment management located in Nigeria, and focuses on the transformative power of technology in Africa. Details of Silicon Badia’s and Digame’s shareholding in the company are not known at the moment. As both of them invested in the early funding rounds, they can expect an excellent return on investment after Swvl’s merger with the Queen’s Gambit Growth Capital SPAC.

Arzan VC, Raed Ventures, Oman Technology Fund, and Sawari Ventures

Arzan Venture Capital, based in Dubai, and the Oman Technology Fund invested in Swvl’s Series A and, B-1 and B-2 rounds. Raed Ventures, which partners with exceptional founders building breakthrough companies and creating scalable impact in MENA region, based in Riyadh, participated in both the Series A and B-1 funding rounds. Sawari Ventures, from the home country of Swvl’s founders, Egypt, is investing in technology companies, across the ICT, hardware, education, healthcare, cleantech and fintech spheres, in the MENA region. Sawari ventures invested in the Series B-1 and Series B-2 rounds.

These four investors do not hold substantial portions of Swvl’s shares but will still enjoy a good return on investment and gain reputation from holding a listed unicorn in their portfolios.

Other institutional investors

As Swvl did not announce all if its funding rounds, not all investors are known. Some of them are Alcazar Capital, Blu Stone Management, Dash Ventures, Endeavor Catalyst, MSA Capital, and Autotech Capital.

Individual investors

There is also a number of individual investors, of which only a few are public. One of them is the founder of Property Finder in Dubai, Michael Lahyani, who invested in Series B-2.

Who is Queen’s Gambit?

Queen’s Gambit Growth Capital has been set up in December 2020 by Victoria Grace, who is founding partner of Colle Capital Partners I, LP (2015), an early-stage technology venture fund in the U.S., which has made investments in a diverse portfolio of 48 companies across the logistics, healthcare, financial technology, marketplace and emerging technology sectors. Prior to that, among other positions, Victoria Grace was a partner at Wall Street Technology Partners LP, a mid-stage technology fund, from November 2000 to February 2014, and a director of Dresdner Kleinwort Wasserstein Private Equity Group from November 2000 to October 2004. Grace serves as the CEO of Queen’s Gambit. Grace co-founded, co-managed and served as President of Work It, Mom! LLC, a network site for professional moms with an advertising revenue model from 2007 until its merger with another content company in 2012

When creating Queen’s Gambit Growth Capital, Grace surrounded herself with a female team, all of them with a proven track record in their own industry.

Anastasia Nyrkovskaya, CFO of Queen’s Gambit, currently acts as the CFO of Fortune Media (USA) Corporation, where she is responsible of finance and accounting, board relations, corporate development, and multiple new initiatives, and a post-acquisition transition. Prior to Fortune Media, Anastasia served as Chief Financial Officer and Treasurer of Birchbox Inc, and as Chief Financial Officer of XpresSpa Group, Inc. (NASDAQ: XSPA), leading finance and accounting functions, including SEC reporting and debt raises in the public markets.

The Board of Nominee Directors comprises;

Jennifer Barbetta (COO at Starwood Capital Group, Artisan Partners Asset Management Inc., with focus on corporate governance; previously Partner and Managing Director at Goldman Sachs, among others);

Cheryl Martin, Ph.D (Founder and Principal of Harwich Partners, LLC, focus on designing and implementing solutions for complex problems, especially those related to energy, sustainability and technology adoption; previously member of the Managing Board of the World Economic Forum in Geneva, Switzerland, where she was responsible for a range of industry and innovation initiatives, previously Cheryl served as Acting Director of the U.S. Department of Energy’s Advanced Research Projects Agency–Energy (“ARPA-E”), among others);

Jill Putman (currently CFO at Jamf Holding Corp. (NASDAQ: JAMF) since 2014; previously CFO of Kroll Ontrack, Inc., a private-equity owned e-discovery firm, previously Divisional CFO and Vice President of Finance at Lifetouch Inc Jill also served as as Vice President of Finance at McAfee Corp., among other positions);

Jeannine Sargent (currently serves in investment and advisory roles that are focused on industries ranging from AI-enabled solutions to energy and sustainability, incl. Breakthrough Energy Ventures, Generation Investment Management LLP, and Katalyst Ventures Management LLC., formerly, she was an EIR/Venture Advisor at Crosslink Capital, among other positions);

Lone Fonss Schroder (currently serves as CEO of Concordium AG, Switzerland, the world’s first blockchain with protocol-level identity mechanism, Lone also sits on the boards of directors of IKEA Group, Volvo Car Group, Aker Group (comprised of Akastor ASA and Aker Solutions ASA which merged with Kvaerner ASA in November 2020), the CSL Group Inc. and Geely Sweden Holdings and previously served as Chairman of Saxo Bank A/S, she formerly served on the boards of a number of other Swedish banks and financial companies and the Finnish carmaker Valmet, among others);

Elizabeth K. Weymouth (Founder, Managing Partner and Chair of the Investment Committee at Grafine Partners, LP, a boutique alternative asset management firm, formerly she served as a Partner at Riverstone Holdings LLC, a private investment firm focused on growth capital investments in the energy industry, formerly Elizabeth served at J.P. Morgan in a variety of roles from 1994 to 2007, including serving as Managing Director at J.P. Morgan Private Bank and Head of Investments for the U.S. Northeast region, among posts with other companies).

Sources: S.E.C., SpacInsider, PR Newswire, menabytes

Important note:

SPAC Consultants is not offering and/or providing investment advisory services in the sense of regulated investment advisory services as per respective EU Directives and their implementation into national law of EU Member States. Instead, SPAC Consultants offers SPAC Project Management services and consults regarding the general principles of US SPACs and their business structuring. Any investment, legal and financial advice that may become necessary for possible sponsors and investors at advanced stages will be provided by the network partners of SPAC Consultants.