Morgan Stanley estimates that the roughly USD $350 Billion global space industry to surge to over USD $1 Trillion by 2040. The Asgard SPAC will be a part of this industry.

The telecommunications industry represents growth, innovation, and disruption for all sectors across the globe.

The COVID-19 pandemic has highlighted the importance of telecom to our lives, highlighted by the massive shift to working from home.

By the end of this decade, 5G could add trillions of dollars to the global economy according to a new report by the McKinsey Global Institute. By 2030, they forecast 5G deployments using millimetre wave spectrum will cover 25% of the global population, at an estimated cost of $700 billion to $900 billion.

The global IoT market size was at $330.6B in 2020. It is expected to reach $875B by 2025, at a CAGR of 27%.

The excellent management team of the Asgard SPAC will be looking at high-tech companies with a positive cash-flow to take the best of it public.

The Asgard SPAC presentation:

SPAC Consultants: Our holistic approach to SPACs

As experienced SPAC consultants or SPAC advisors, we provide our SPAC advisory and project management services to different group of clients related to SPACs.

Our SPAC consulting and project management services are tailor-made for private equity investors who wish to invest in their own SPAC on the pre-IPO stage as so-called SPAC Sponsors, or who prefer to sponsor an existing SPAC project at its pre-IPO stage.

As SPAC consultants, we are designing and structuring SPACs, arranging for S.E.C. approval and listing at Nasdaq or NYSE, organising pre-IPO roadshows, arrange for IPOs and assist in finding acquisition targets as per a SPAC’s acquisition strategy. Our SPAC consultants and advisers are well experienced on all stages and aspects of SPACs.

If you are interested in setting up a SPAC or in participating in an existing SPAC on its pre-IPO stage, we will be happy to arrange an initial Zoom conference to get acquainted, to further elaborate on SPACs and their manifold opportunities, and to discuss with you your SPAC investment and business ideas.

Important note:

SPAC Consultants is not offering and/or providing investment advisory services in the sense of regulated investment advisory services as per respective EU Directives and their implementation into national law of EU Member States. Instead, SPAC Consultants offers SPAC Project Management services and consults regarding the general principles of US SPACs and their business structuring. Any investment, legal and financial advice that may become necessary for possible sponsors and investors at advanced stages will be provided by the network partners of SPAC Consultants.

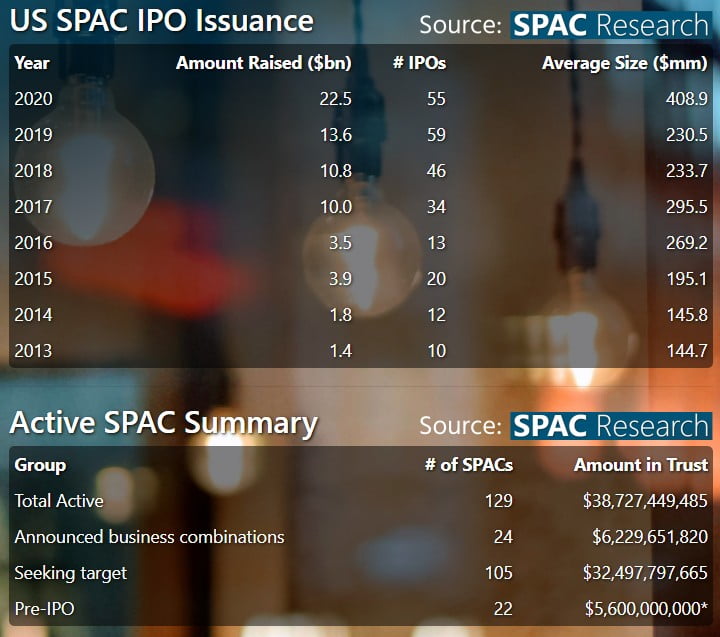

A total of 295 SPACs floated their IPO during the first quarter of 2021, compared with 128 SPACs IPOs during the second half of 2020. To our opinion, in 2021, we will see a total of around 800 – 900 SPAC IPOs in the United States, plus a very few in Europe and even less in Asia. But let us see how the market will develop, how some speculative and over-tuned SPACs will influence the market, and what regulation changes might come up to tame speculators and other wrongdoers. Whatever this year will show, one thing is clear: SPACs are here to stay. At least as long as we continue with quantitative easing, low or negative interest rate and general economic uncertainty. And that means long years to go.

SPAC Acquisition Target Sectors

It is not easy to do a meaningful evaluation and grouping of acquisition target industries, as almost everything today is related to technology. In our evaluation, we put those SPACs into the “Tech” category that explicitly mention in the acquisition strategy “tech company”, “biotech”, “fintech” etc. Where the acquisition strategy of a SPAC included several criteria, we chose the one which seemed to be the main criteria, or which appeared as the most specific area.

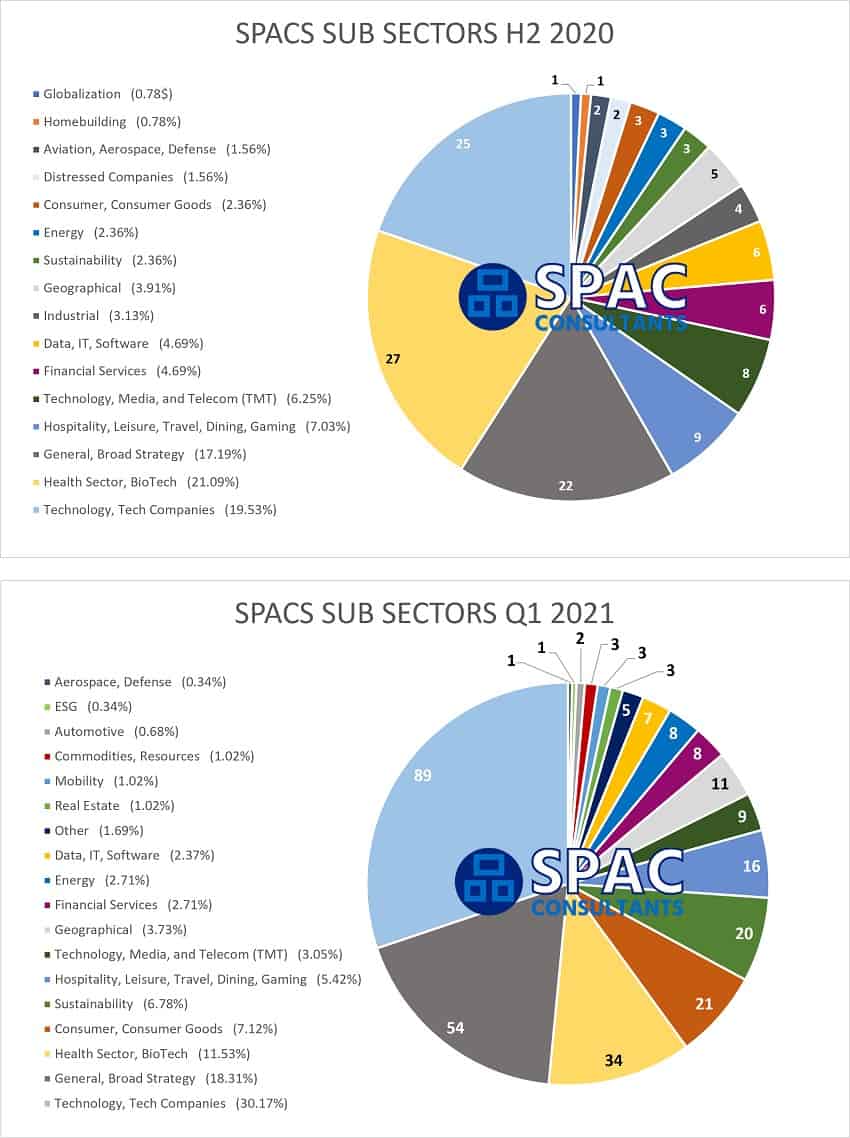

While the share of tech companies was 31.25% of all SPACs that launched their IPO in H2 2020 (40 of 128 SPACs), tech companies’ share increased to 46.78% in Q1 2021 (138 of 295 SPACs). It seems that the SPAC frenzy in 2021 did also lead to a frenzy in hunting for even higher growth potential. We did already witness some exaggeration in target company valuations by SPACs, when mature startups with no or very little cashflow were appreciated at a billion dollar and more. Such “hyper-valuations” will make it difficult for the target company to deliver accordingly, once taken public by through merger with a special-acquisition company.

The second largest group of acquisition target industries or sectors in both H2 2020 and Q1 2021 comprises sectors that we commonly names as “Social”. This group includes acquisition target sub-sectors that have a focus on dealing with people of having a direct impact on people through technology, such as “Consumer, Consumer Goods”, “Energy”, “ESG” (meaning target companies with a focus on Environmental, Social, and Corporate Governance, which could be from any industry), “Financial Services “, “Hospitality, Leisure, Travel, Dining, Gaming”, “Mobility” and “Sustainability”.

This group of target industries had a share of 26.56% in H2 2020 (34 of 128 SPACs), which then sized down to 19.32% in Q1 2021 (57 of 295 SPACs).

The third largest share in both H2 2020 and in Q1 2021 goes to SPACs that did define their acquisition strategy in their Registration Statement (S-1) filed with the Security Exchange Commission in a very general and broad way not allowing a conclusion that would lead to any specific industries. The share of the group “General, Broad Strategy” is 17.19% in H2 2020 (22 of 128 SPACs) and, almost unchanged, 18.31% in Q1 2021 (54 of 295 SPACs).

The sector group “Others” includes all those sectors with a share of 2% or less.

SPAC Acquisition Target Sub-Sectors

As perhaps to be expected, technology and tech companies take a big piece of the cake, namely 19.53% in in H2 2020 (25 of 128 SPACs) and 30.17% in Q1 2021 (89 of 295 SPACs).

However, we separated Biotech companies. Although biotech companies are still tech companies, they form the largest part of tech companies in general and thus we gave them their own piece of the cake. The sub-sector “Health Sector, Biotech” does also include a few acquisition strategies that focus on health care. During H2 2020, the sub-sector health and biotech took a share of 21.09% (27 of 128 SPACs), and in Q1 2021 a share of 11.53% (34 of 295 SPACs).

FinTech companies in the focus of SPAC acquisition strategies, which are not mentioned separately in our evaluation, took a share of 4.65% with just 6 SPACs in H2 2020, and a share of 6.05% with 18 SPACs in Q1 2020. This just mentioned because we often hear that Fintechs are the darling of SPACs.

We actually love to see that increase of the focus on Fintechs and would love to see an increase in SPACs focusing on financial services. Fintechs are the technologies that will disrupt financial services, and re-organisation of financial services is a way of making banking easier for everybody, and a way of more banking democracy, providing better banking access to the under-banked.

The increase of SPACs with an acquisition strategy focusing on consumers and consumer goods is interesting, to our opinion. While 2.36% of the SPACs during H2 2020 focused on this topic, we see 7.12% of the SPACs in Q1 2021. These SPACs will focus on consumer behaviour, related mass data and its utilisation for the refinement of marketing strategies and tools.

Interesting is also the geographical focus of some SPACs, most of them not even mentioning any specific industry. In 2020, two SPACs mentioned in their acquisition strategy that they are focusing on Asia, and one SPAC each focuses on Mexico, Brazil, and Europe. In 2021, the geographical distribution was as following: two SPACs focusing on Africa (both with ESG as secondary criterion), one on Asia, one on Brazil, two on China, two on Europe and North America, one on the EMEA region, one on North America, and one SPAC mentioned that it focuses on anywhere outside of the US.

Source of base data for this article: SPAC Insider.

Conclusion

Technology and tech companies are paving the way to our future. The entire tech development is just at its beginning, areas like Mass Data, AI, Fintech, or Biotech, to name a few, will disrupt things as we did them until now (or yesterday) and will form new ways to deal with things, improving our lives. It is therefore only natural that technology and tech companies represent the lion portion of all SPAC IPOs. The expectable growth potential further adds to the interest of SPACs in technology and tech companies.

On the other hand, we love the diversification of SPAC acquisition strategies, allowing companies other than only tech companies to go public and to get access to funds for their projects and ambitions. It is creating hope for our future that topics like Environmental, Social, and Corporate Governance (ESG), Sustainability, Healthy Living and Education took already place among the many focuses of SPAC acquisition strategies.

Never in history have so large private funds been provided to the economy and to companies in such a short period. If not misused but structured and invested professionally, SPACs are and will be one of the driving powers of economic, technologic, and social development.

Shanda Consult has been working with SPACs for many years, and our network of SPAC executives has deep experience in the sector. If you need to learn more about how to successfully use a SPAC structure and perhaps wish to set up your own SPAC, we are here to help.

Please contact us with any questions you may have.

Nicosia, Cyprus, April 02, 2021.

Important note:

SPAC Consultants is not offering and/or providing investment advisory services in the sense of regulated investment advisory services as per respective EU Directives and their implementation into national law of EU Member States. Instead, SPAC Consultants offers SPAC Project Management services and consults regarding the general principles of US SPACs and their business structuring. Any investment, legal and financial advice that may become necessary for possible sponsors and investors at advanced stages will be provided by the network partners of SPAC Consultants.

HAIMA will focus on acquisitions in Microbiome, Therapeutics, Diagnostics, Pre & Probiotics and Nutrition.

Interested and ambitioned founders are welcome to participate, please contact us through the contact form below.

The human microbiome is collectively all microbes in the human body (good & bad microbes).

Disbalance (dysbiosis) between good & bad microbes is the cause of many diseases like cancer, atherosclerosis, diabetes, obesity etc.

The HAIMA SPAC’s acquisition strategy focuses on the the addressable microbiome market, which has a volume of USD 2.2bn as per 2020. The main market is the US, followed by the EU.

Growth drivers are;

- Rising incidence of lifestyle-related diseases like CVD, Diabetes, IBS;

- Personalized nutrition awareness;

- Increase in autoimmune disorders and antibiotic resistance.

HAIMA aims to generate synergies with additional acquisitions in the wound care market, a market with an addressable volume of USD 22bn, The main market is again the US, followed by the EU.

Growth drivers in this market are:

- Aging population;

- Rising incidences of diabetes, obesity and other chronic conditions;

- Increasing surgical interventions leading to acute wound care;

- Growing awareness of active wound products;

- Increasing number of seniors living in long-term care facilities.

The HAIMA presentation:

SPAC Consultants: Our holistic approach to SPACs

As experienced SPAC consultants or SPAC advisors, we provide our SPAC advisory and project management services to different group of clients related to SPACs.

Our SPAC consulting and project management services are tailor-made for private equity investors who wish to invest in their own SPAC on the pre-IPO stage as so-called SPAC Sponsors, or who prefer to sponsor an existing SPAC project at its pre-IPO stage.

As SPAC consultants, we are designing and structuring SPACs, arranging for S.E.C. approval and listing at Nasdaq or NYSE, organising pre-IPO roadshows, arrange for IPOs and assist in finding acquisition targets as per a SPAC’s acquisition strategy. Our SPAC consultants and advisers are well experienced on all stages and aspects of SPACs.

If you are interested in setting up a SPAC or in participating in an existing SPAC on its pre-IPO stage, we will be happy to arrange an initial Zoom conference to get acquainted, to further elaborate on SPACs and their manifold opportunities, and to discuss with you your SPAC investment and business ideas.

Important note:

SPAC Consultants is not offering and/or providing investment advisory services in the sense of regulated investment advisory services as per respective EU Directives and their implementation into national law of EU Member States. Instead, SPAC Consultants offers SPAC Project Management services and consults regarding the general principles of US SPACs and their business structuring. Any investment, legal and financial advice that may become necessary for possible sponsors and investors at advanced stages will be provided by the network partners of SPAC Consultants.

HEIDI, a SPAC focusing on the acquisition of promising companies with forward-looking technologies and a track-record in smart energy production or distribution.

SMART ENERGY

To manage energy consumption from production to end-user and beyond:

- HEIDI aims for nothing less than to be complete integrated power network with highest standard of convenience.

- Artificial Intelligence (AI) will control on-demand production of electric power. Alongside HEIDI will be providing personalized heating and lighting applications based on a specified user behavior.

- Combined renewable energy, smart grid, cross-platform usability and power conscious usage-controlled AI and managed by blockchain technology will take the energy transition a decisive step forward.

SMART POWER = ENERGY OF THE FUTURE

- Without any doubt, energy consumption will increase each year

despite of massive efforts to save energy. - Resources decline and grid capacity is to most extend limited.

- Political decisions and social changes exacerbate market conditions.

- Users like to have for a more convenient and safer living environment.

- At the same time there is a demand for constant prices for electric power.

The strategy of HEIDI

- Use existing energy resources wise and distribute energy on demand;

- Tracking users’ behavior of the past by Blockchain technology;

- Forecast demand in individualized and more defragmented markets by Artificial Intelligence;

- Producing renewable energy to be relatively independent.

Gathering Big Data en passé from users’ behavior will form a second leg for HEIDI’s business model.

The Market

Worldwide market for Smart Home will be USD 108 billions in 2022 with a CAGR of 25%.

European Smart Grid will be USD 30 bn at the same time; worldwide annual revenue will be more than USD 70 bn.

Adding renewable energy, in five years the market for HEIDI will be clearly above USD 180 bn worldwide with CAGR of 4.8% to 27%, depending of sector and region.

E-Mobility has not been taken into account in this calculation but could be added to this SPAC.

INVESTMENT, TARGETED IPO PROCEEDS & ACQUISITION VALUE

Given that other market participants are financially strong, and given that HEIDI has a broad approach, the pre-IPO investment should not be less than USD 15 millions.

Thus, IPO-proceeds are likely to reach USD 250 to 300 millions and enable HEIDI to acquire companies worth USD 700 M to USD 1.1 B in the best-case scenario.

The HEIDI presentation:

SPAC Consultants: Our holistic approach to SPACs

As experienced SPAC consultants or SPAC advisors, we provide our SPAC advisory and project management services to different group of clients related to SPACs.

Our SPAC consulting and project management services are tailor-made for private equity investors who wish to invest in their own SPAC on the pre-IPO stage as so-called SPAC Sponsors, or who prefer to sponsor an existing SPAC project at its pre-IPO stage.

As SPAC consultants, we are designing and structuring SPACs, arranging for S.E.C. approval and listing at Nasdaq or NYSE, organising pre-IPO roadshows, arrange for IPOs and assist in finding acquisition targets as per a SPAC’s acquisition strategy. Our SPAC consultants and advisers are well experienced on all stages and aspects of SPACs.

If you are interested in setting up a SPAC or in participating in an existing SPAC on its pre-IPO stage, we will be happy to arrange an initial Zoom conference to get acquainted, to further elaborate on SPACs and their manifold opportunities, and to discuss with you your SPAC investment and business ideas.

Important note:

SPAC Consultants is not offering and/or providing investment advisory services in the sense of regulated investment advisory services as per respective EU Directives and their implementation into national law of EU Member States. Instead, SPAC Consultants offers SPAC Project Management services and consults regarding the general principles of US SPACs and their business structuring. Any investment, legal and financial advice that may become necessary for possible sponsors and investors at advanced stages will be provided by the network partners of SPAC Consultants.